If you or someone you love is on a Medicare Advantage plan, the ground just shifted under your feet — and most people don’t yet realize it.

A peer-reviewed research letter published in JAMA in February 2026, from a team at the Johns Hopkins Bloomberg School of Public Health, put a hard number on what many of us in this business have been watching unfold: roughly 2.9 million Medicare Advantage members — about 1 in 10 — are being forced out of their plans for 2026. Their insurance company either pulled out of the county entirely or shut down the plan they were on.

For context, the historical rate of forced disenrollment ran at about 1% from 2018 through 2024. It jumped to 6.9% in 2025, and now sits at 10% for 2026. That’s a tenfold increase in two years.

Why This Is Happening

The short version: several large insurers looked at rising medical costs and shifting federal payment rules, and decided they couldn’t make the Medicare Advantage math work in certain markets anymore. So they cut plans. Some smaller carriers exited entirely.

The people hit hardest, according to the research, were enrollees in PPO plans, plans from smaller carriers, plans with lower star ratings, and rural counties. If any of that describes your current plan, you should assume you’re closer to this problem than farther from it.

What Happens Next If You Get Forced Off Your Plan

Here’s the part almost no one talks about until it’s too late.

When your Medicare Advantage plan exits your county, you typically get a Special Enrollment Period to pick a new plan. That sounds like a solution. In many cases it isn’t.

Your options usually break down into three uncomfortable choices:

Enroll in a different Medicare Advantage plan — often one with a narrower network, a different provider list, and different drug coverage. Your current doctors may or may not be in-network. Your prescriptions may or may not be covered the same way.

Go back to Original Medicare — which covers about 80% of costs, leaving you exposed to the remaining 20% with no annual out-of-pocket cap. That’s why most people on Original Medicare add a Medicare Supplement (Medigap) plan to fill the gap.

Go back to Original Medicare and try to buy a Medigap plan — this is where the catch lives.

The Medigap Catch That Blindsides People

Federal law protects your right to buy any Medigap plan sold in your state, with no health questions asked, during a specific one-time six-month window that starts when you’re first 65 and enrolled in Medicare Part B.

If you missed that window because you went straight into Medicare Advantage, and you now need a Medigap plan because your Advantage plan disappeared, in most states the insurance company can look at your health history and either turn you down or raise your rate.

There are some situations that create guaranteed-issue rights — protected windows where you can buy Medigap without medical underwriting. Losing your Medicare Advantage plan because it exited your area is one of them. But the timing is tight (typically 63 days after your coverage ends) and the plans you’re guaranteed access to are a narrower set than you’d have during the original Open Enrollment Period.

This is why I’ve said for years, and will keep saying: the decision to enroll in Medicare Advantage isn’t fully reversible. It looks like a low-cost option going in. When the exit door slams shut, the underwriting door often does too.

What Medicare Beneficiaries Should Do Right Now

If you’re on a Medicare Advantage plan, here’s the checklist I’d walk any client through:

Read your Annual Notice of Change carefully. This letter comes every fall. It tells you whether your plan is continuing, changing, or exiting for the coming year.

Check whether your doctors and prescriptions are still covered. Even if your plan continues, the network and formulary can change year to year.

Know your guaranteed-issue rights. If your plan is exiting your area, you have a limited window to buy certain Medigap plans without health underwriting. Don’t miss it.

Talk to someone who doesn’t sell Medicare Advantage. I don’t. That’s a deliberate choice, not an oversight. If you’re getting advice only from someone who does, you’re getting one side of the picture.

Why I Don’t Sell Medicare Advantage

The Johns Hopkins study is the clearest third-party validation I’ve seen of the position I’ve held since day one of my practice. Medicare Advantage plans are heavily marketed, often with no monthly premium and extra perks that sound great. What the commercials don’t tell you is that the insurance company can leave the market and take your coverage with them — and once your health changes, getting back to Original Medicare with a supplement can be difficult or impossible.

I stick to Medicare Supplement plans, where you keep your own doctors, there’s no network to fight, and the coverage doesn’t disappear when a carrier decides a county isn’t profitable enough.

If You’re Reading This Because Your Plan Just Got Canceled

Don’t panic, but don’t wait either. Your guaranteed-issue window is real but limited. Call or text me at (623) 742-3878 (Arizona) or (910) 760-2124 (North & South Carolina) and let’s talk through what you actually qualify for right now. There’s no cost for the conversation, and I’ll tell you plainly whether a Medigap plan is a good fit for your situation — including when it isn’t.

Source: Meiselbach MK, Lavallee M, Xu J, Polsky D. “Forced Disenrollments Among Medicare Advantage Beneficiaries Following 2026 Plan Exits.” JAMA, February 18, 2026. Johns Hopkins Bloomberg School of Public Health.

If you’re shopping for a Medicare Supplement in North Carolina, there’s one enrollment window that matters more than almost any other — and most people don’t find out about it until it’s already closed. I’m licensed here in North Carolina and South Carolina, and Medicare Supplement North Carolina questions are among the ones I get asked most. So let me walk you through it plainly.

What the Medicare Supplement North Carolina open enrollment window actually is

Your Medicare Supplement (Medigap) Open Enrollment Period is a one-time, six-month window. It starts the month you’re both 65 or older and enrolled in Medicare Part B. During those six months, insurance companies in North Carolina have to sell you any Medigap plan they offer, no matter your health history. They can’t turn you down, they can’t charge you more because of a health condition, and they can’t make you wait out a pre-existing condition.

That’s a powerful protection. It’s also temporary.

What changes after the window closes

Once those six months are up, the rules flip. Insurance companies in North Carolina can use medical underwriting — which means they get to look at your health history and decide whether to accept you, and at what price. A condition you didn’t think twice about can suddenly mean a higher premium, or a flat denial.

I want to be honest with you about this, because it’s the part that catches people off guard: waiting isn’t free. The healthy time to lock in a Medigap plan is during that first window, before anything on your medical record gives a company a reason to say no.

Turning 65 later? North Carolina has a rule worth knowing

Here’s something specific to our state that a lot of folks miss. If you qualified for Medicare under 65 due to a disability, North Carolina law guarantees you access to certain Medigap plans — Plans A, D, and G — even before you turn 65. And then, when you do reach 65, you get a brand-new, full six-month Open Enrollment Period to buy any standardized plan at the standard rate, with no health screening at all.

That fresh window at 65 is a genuine second chance, and it’s written into state law. Not every state offers it. If this is your situation, don’t let that window slip by the way the first one might have.

What if you already missed your window?

Don’t panic. Missing your Open Enrollment Period doesn’t mean you’re out of options — it means the path looks different. You can still apply for a Medigap policy any time; the company just gets to underwrite it. Depending on your health, you may still qualify at a good rate. And in certain situations, you may have guaranteed-issue rights that reopen a protected window — for example, if you lose other coverage.

This is exactly the kind of thing worth a quick phone call before you assume the door is shut. There are 48 companies selling Medigap plans in North Carolina, and because the plans are standardized, a Plan G is a Plan G no matter whose name is on it — so the real work is finding the company that will take you at the best price.

Why I don’t sell Medicare Advantage

You’ll notice I keep talking about Medigap, not Medicare Advantage. That’s on purpose. I don’t sell Medicare Advantage plans, and I don’t plan to start. I’ve watched too many people get pulled in by a low premium, then run into network restrictions and denied care right when they needed the plan to work. Even here in North Carolina, major health systems have been walking away from some Advantage plans. I’d rather offer you coverage I’d put my own family on.

Let’s figure out your Medicare Supplement North Carolina options together

Whether you’re coming up on 65, already past your Open Enrollment Period, or just not sure where you stand, I’m happy to sort it out with you — by phone, text, or email, whatever’s easiest. There’s no cost to work with me, and the rate is the same as going direct. I work for you, not the insurance company.

Call or text me at (910) 760-2124, or email Andy@coastalcarolinahealth.com. A real person answers — no call centers.

American Insurance Benefits Now Serves North Carolina and South Carolina

For nearly 25 years, I’ve been helping Arizona families cut through the confusion of health insurance shopping — comparing plans honestly, explaining the fine print, and making sure nobody gets stuck with coverage that doesn’t actually work when they need it. Today, I’m excited to share that I’m expanding that same approach to North Carolina and South Carolina.

I’m now licensed and ready to help clients in North Carolina and South Carolina, in addition to Arizona.

Why I’m Expanding to North Carolina and South Carolina

I split my time seasonally between Arizona and North Carolina, so this isn’t a broker calling in from across the country — it’s someone who spends real time in both markets. That matters, because health insurance is local. Carrier networks, plan availability, and pricing all vary by state, and the best plan for a client in Surprise, Arizona often looks nothing like the best plan for someone in the Carolinas.

What Stays the Same

Whether you’re in Arizona, North Carolina, or South Carolina, the way I work with clients doesn’t change:

Independent, not captive. I compare plans across many top carriers, not just one company’s product line, so you get an honest side-by-side comparison.

Always free to you. I’m paid by the carrier, not by you. Your premium is exactly the same whether you use a broker or go direct.

No Medicare Advantage. I don’t sell it, and I’ll explain why Medicare Supplement often protects you better over the long run.

PPO alternatives and Short-Term Medical. For healthy clients who don’t need a full ACA plan’s price tag, these options can mean real savings without giving up broad provider access.

Everything by phone, text, or email. No office visits required, no automated systems, no spam calls — just a straightforward conversation.

North Carolina and South Carolina: What’s Different

For Arizona clients, I continue to specialize in finding private plans that keep Mayo Clinic in-network — something most standard ACA plans exclude entirely. For clients in North Carolina and South Carolina, I bring that same careful attention to your local carrier networks and plan options.

Get Started

If you’re in Arizona, call or text me at (623) 742-3878. If you’re in North Carolina or South Carolina, reach me at (910) 760-2124. Or head to azhealth.us to request a free quote.

I look forward to helping more families get covered — without the stress, and without the sales pitch.

If you’re feeling the ACA subsidy cliff hit your premium this year, you’re not imagining things. The enhanced subsidies that kept Marketplace premiums manageable from 2021 through 2025 expired at the end of last year, and the ACA subsidy cliff is back in force for 2026 at the original 400% federal poverty level cutoff. For a single person, that cutoff sits around $62,600 in income. Cross it by even a dollar, and your premium tax credit disappears completely — not reduced, gone. You can check the current federal poverty level thresholds directly at healthcare.gov.

I’ve had a lot of calls this year from Arizona clients who did everything right at open enrollment and are still stunned by what showed up on their bill in month two or three. So let’s talk about what your actual options are right now, mid-year, if you’re one of them.

The ACA Subsidy Cliff: What You Can and Can’t Do

The federal Marketplace only reopens outside of open enrollment if you have a qualifying life event — losing other coverage, getting married, having a baby, or a permanent move, among a few others. Deciding you can no longer afford your plan isn’t a qualifying event. Neither is getting dropped for non-payment. So if you’re already enrolled and the ACA subsidy cliff caught you, you generally can’t just walk back into the Marketplace and pick something cheaper.

That doesn’t mean you’re stuck with your current plan, though. It means the fix has to come from somewhere other than the Marketplace itself.

Off-Exchange Plans Are Worth a Look

Here’s something a lot of people don’t realize: ACA-compliant plans are available off-exchange, year-round, directly through carriers or through a broker like me. If you landed above the 400% cliff, you weren’t getting a subsidy anyway — so an off-exchange plan gives you the same coverage rules and often the same network, without needing a special enrollment period to switch into it. For households in exactly your situation, this is usually the cleanest path.

PPO Alternatives Deserve a Serious Look Too

This is where I spend most of my time with clients right now. If you’re relatively healthy and rarely use your coverage beyond routine visits, a full ACA plan priced at full freight may not be the best use of your money. Short-term medical and PPO alternative plans can offer meaningfully lower premiums with broad provider networks — including, in the right plan, access to Mayo Clinic, which most standard ACA plans exclude entirely. These aren’t a fit for everyone, and I’ll tell you honestly if they’re not a fit for you. But for a lot of Arizona families right now, they’re the difference between coverage they can actually afford and coverage they’re quietly resenting every month.

If You’re Close to the Cliff, Watch Your Income

If your income is hovering right around that 400% line, a few strategies can help you stay under it — and they’re worth knowing about before year-end, not after:

HSA contributions reduce your ACA-specific modified adjusted gross income (MAGI). As of this year, all Bronze Marketplace plans are HSA-eligible, which opens this option to more people than before.

Traditional IRA contributions work the same way — they lower MAGI, which is what your subsidy eligibility is actually based on.

Qualified Roth withdrawals don’t count toward MAGI at all, so if you need to supplement income mid-year, pulling from a Roth won’t push you closer to the cliff the way other income sources will.

If you’re self-employed or your income varies month to month, it’s worth tracking your estimated MAGI throughout the year rather than waiting until tax time to find out you went over. Going over the line even briefly can mean paying back subsidies you already received.

The Real Mistake to Avoid

The biggest mistake I see is people treating “alternative coverage” as a straight swap for their old ACA plan. It isn’t, and it shouldn’t be sold to you that way. A full ACA plan bundles preventive care, specialist visits, hospitalization, and prescription coverage into one plan with a managed deductible. A short-term or PPO alternative plan works differently, and figuring out whether it actually covers what you need takes an honest conversation — not a sales pitch.

Beat the ACA Subsidy Cliff: Let’s Look at Your Numbers

Every household’s situation here is different — your income, your health, which doctors you need to keep, and how close you are to that 400% line. If your premium jumped this year and you want an honest second opinion on what else is out there, I’m happy to walk through it with you. No pressure, no cost, and I’ll tell you plainly if your current plan is still your best option.

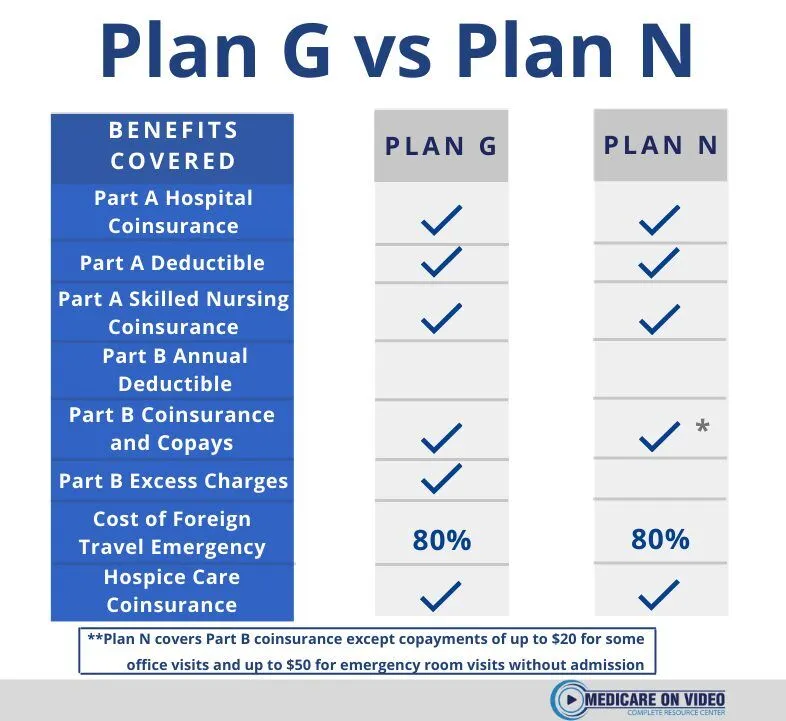

Plan G vs Plan N — when choosing a Medicare Supplement plan in Arizona, this is the comparison that matters most. Both plans are popular. Both cover most of what Original Medicare leaves behind. However, they handle office visits and cost-sharing differently. In this guide, you’ll see exactly how Plan G vs Plan N compares — so you can choose the right plan for 2026.

What Plan G and Plan N Both Cover

First, it helps to know what these two plans share. Both Plan G vs Plan N cover the following:

Medicare Part A coinsurance and hospital costs

Medicare Part A deductible ($1,676 in 2026)

Medicare Part A hospice care coinsurance

Skilled nursing facility coinsurance

Medicare Part B coinsurance — with one key difference explained below

Foreign travel emergency care up to plan limits

In addition, both plans require you to pay the Part B deductible ($257 in 2026) once per year. After that, coverage kicks in. So far, they look nearly identical. The differences, however, matter a lot depending on how often you use your insurance.

Plan G vs Plan N: The Key Differences

Plan G covers 100% of your Medicare Part B coinsurance. Therefore, after your Part B deductible, you owe nothing for covered outpatient care.

Plan N covers most Part B coinsurance — but not all. Specifically, Plan N has these out-of-pocket costs:

Up to $20 copay per office visit

Up to $50 copay per emergency room visit (waived if admitted)

Part B excess charges — if a doctor doesn’t accept Medicare assignment, you pay the difference between their rate and Medicare’s approved amount

Most Arizona doctors accept Medicare assignment. As a result, excess charges rarely come up. However, the office visit copays do add up if you see doctors often. That’s the core of the Plan G vs Plan N decision.

How Premiums Compare in Arizona

Plan N typically costs $20–$40 less per month than Plan G in Arizona. Therefore, over a full year, you could save $240–$480 in premiums with Plan N.

However, that savings only holds if your copays stay below the premium difference. For example, if you visit the doctor six times per year, that’s up to $120 in Plan N copays. In that case, Plan N still wins on price. On the other hand, frequent visits or ER trips can close the gap quickly.

The bottom line: run the numbers for your situation. That’s exactly what I do for clients at no charge.

Who Should Choose Plan G

Plan G makes the most sense in these situations:

You have ongoing health conditions or frequent doctor visits

You want predictable costs with no copay surprises

You travel often and may see out-of-network providers

You simply want the most comprehensive coverage available

In short, Plan G is the “set it and forget it” option. After your Part B deductible, your costs are done for the year.

Who Should Choose Plan N

Plan N works well in these situations:

You are generally healthy and see a doctor only a few times per year

You want to lower your monthly premium

Your doctors all accept Medicare assignment

You are comfortable paying a small copay at visits

Furthermore, Plan N is a smart choice for people who want solid Medigap coverage without paying for benefits they rarely use.

Plan G vs Plan N: Carriers in Arizona

Both plans are standardized by the federal government. Therefore, the benefits are identical no matter which insurance company you buy from. What differs between carriers is the monthly premium and the company’s rate history.

Whether you choose Plan G or Plan N, timing is critical. When you first enroll in Medicare Part B, you receive a 6-month Medigap open enrollment window. During this period, insurance companies cannot deny you or charge more based on health history.

After this window closes, however, insurers can use medical underwriting. Consequently, pre-existing conditions could affect your options or your premium. This window only happens once. Therefore, if you’re turning 65, get your Medigap plan in place before your birthday month.

I’m Andy Orlikoff, an independent Medicare Supplement broker in Surprise, AZ. I’ve been helping Arizona residents compare Plan G vs Plan N and enroll in the right coverage since 2004. I don’t sell Medicare Advantage — just honest Medigap guidance at no cost to you.

I’ll pull side-by-side quotes from multiple carriers and walk you through the numbers. You decide what fits. I handle the enrollment.

American Insurance Benefits Now Serves North Carolina and South Carolina

American Insurance Benefits Now Serves North Carolina and South Carolina