Medicare Plan G vs Plan N in Arizona: Which One Is Right for You in 2026?

Plan G vs Plan N — when choosing a Medicare Supplement plan in Arizona, this is the comparison that matters most. Both plans are popular. Both cover most of what Original Medicare leaves behind. However, they handle office visits and cost-sharing differently. In this guide, you’ll see exactly how Plan G vs Plan N compares — so you can choose the right plan for 2026.

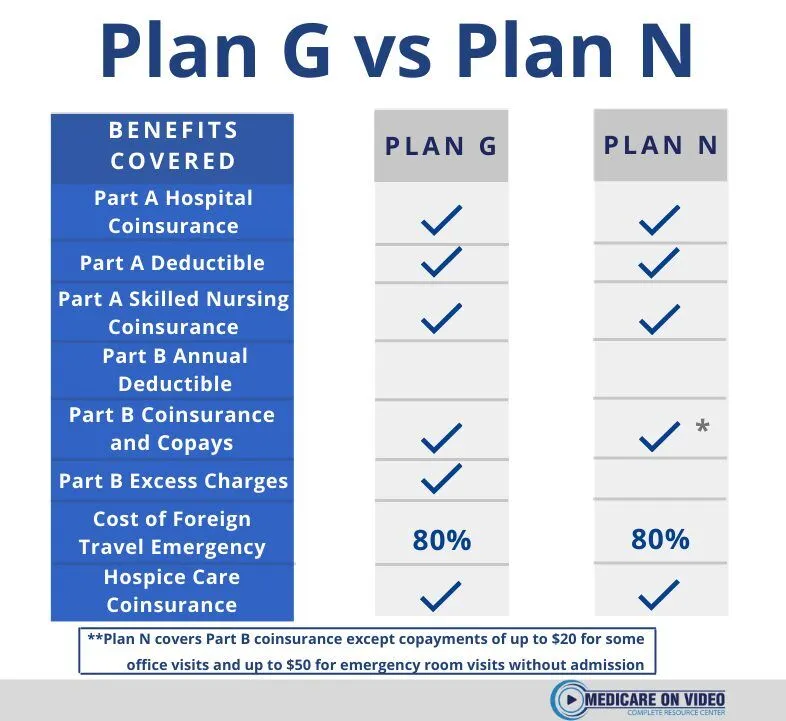

What Plan G and Plan N Both Cover

First, it helps to know what these two plans share. Both Plan G vs Plan N cover the following:

- Medicare Part A coinsurance and hospital costs

- Medicare Part A deductible ($1,676 in 2026)

- Medicare Part A hospice care coinsurance

- Skilled nursing facility coinsurance

- Medicare Part B coinsurance — with one key difference explained below

- Foreign travel emergency care up to plan limits

In addition, both plans require you to pay the Part B deductible ($257 in 2026) once per year. After that, coverage kicks in. So far, they look nearly identical. The differences, however, matter a lot depending on how often you use your insurance.

Plan G vs Plan N: The Key Differences

Plan G covers 100% of your Medicare Part B coinsurance. Therefore, after your Part B deductible, you owe nothing for covered outpatient care.

Plan N covers most Part B coinsurance — but not all. Specifically, Plan N has these out-of-pocket costs:

- Up to $20 copay per office visit

- Up to $50 copay per emergency room visit (waived if admitted)

- Part B excess charges — if a doctor doesn’t accept Medicare assignment, you pay the difference between their rate and Medicare’s approved amount

Most Arizona doctors accept Medicare assignment. As a result, excess charges rarely come up. However, the office visit copays do add up if you see doctors often. That’s the core of the Plan G vs Plan N decision.

How Premiums Compare in Arizona

Plan N typically costs $20–$40 less per month than Plan G in Arizona. Therefore, over a full year, you could save $240–$480 in premiums with Plan N.

However, that savings only holds if your copays stay below the premium difference. For example, if you visit the doctor six times per year, that’s up to $120 in Plan N copays. In that case, Plan N still wins on price. On the other hand, frequent visits or ER trips can close the gap quickly.

The bottom line: run the numbers for your situation. That’s exactly what I do for clients at no charge.

Who Should Choose Plan G

Plan G makes the most sense in these situations:

- You have ongoing health conditions or frequent doctor visits

- You want predictable costs with no copay surprises

- You travel often and may see out-of-network providers

- You simply want the most comprehensive coverage available

In short, Plan G is the “set it and forget it” option. After your Part B deductible, your costs are done for the year.

Who Should Choose Plan N

Plan N works well in these situations:

- You are generally healthy and see a doctor only a few times per year

- You want to lower your monthly premium

- Your doctors all accept Medicare assignment

- You are comfortable paying a small copay at visits

Furthermore, Plan N is a smart choice for people who want solid Medigap coverage without paying for benefits they rarely use.

Plan G vs Plan N: Carriers in Arizona

Both plans are standardized by the federal government. Therefore, the benefits are identical no matter which insurance company you buy from. What differs between carriers is the monthly premium and the company’s rate history.

In Arizona, I compare plans from Physicians Mutual, Mutual of Omaha, BCBS Arizona, and LifeShield National. Premium rates for the same plan can vary by $50–$100 per month between carriers. As a result, comparing quotes before you enroll can save you a significant amount each year.

Enrollment Timing Matters More Than Plan Choice

Whether you choose Plan G or Plan N, timing is critical. When you first enroll in Medicare Part B, you receive a 6-month Medigap open enrollment window. During this period, insurance companies cannot deny you or charge more based on health history.

After this window closes, however, insurers can use medical underwriting. Consequently, pre-existing conditions could affect your options or your premium. This window only happens once. Therefore, if you’re turning 65, get your Medigap plan in place before your birthday month.

For official enrollment guidance, see Medicare.gov’s Medigap enrollment page.

Get a Free Plan G vs Plan N Quote in Arizona

I’m Andy Orlikoff, an independent Medicare Supplement broker in Surprise, AZ. I’ve been helping Arizona residents compare Plan G vs Plan N and enroll in the right coverage since 2004. I don’t sell Medicare Advantage — just honest Medigap guidance at no cost to you.

I’ll pull side-by-side quotes from multiple carriers and walk you through the numbers. You decide what fits. I handle the enrollment.

Call or text: (623) 742-3878

Email: andy@azhealth.us

Fill out the contact form →

Serving Surprise, Phoenix, Peoria, Glendale, Goodyear, Buckeye, Scottsdale, Mesa, Chandler, Gilbert, and all of Arizona.

American Insurance Benefits | 14955 W Bell Rd #8031, Surprise, AZ 85374 | Licensed Arizona Insurance Broker since 1999